The known: Breast hypertrophy causes physical and psycho‐social impairment in women, and breast reduction surgery is the most effective treatment. However, access to surgery is often restricted by health policies that deem it non‐therapeutic, including in Australia.

The new: The first economic evaluation in Australia of breast reduction for women with symptomatic breast hypertrophy indicated that it is cost‐effective for improving their health‐related quality of life ($7808 per quality‐adjusted life‐year).

The implications: Healthcare systems in all Australian states should support access to breast reduction surgery for both private and public patients with symptomatic breast hypertrophy.

Breast hypertrophy affects quality of life and causes physical and psycho‐social problems for women. Breast reduction surgery is highly effective for relieving the pain and functional problems associated with breast hypertrophy and improves health‐related quality of life.1,2,3 However, breast reduction is often regarded as a cosmetic rather than a functional procedure, and health care funders and third party providers restrict access to surgery, despite evidence of its therapeutic benefit.

The Australian Medicare Benefits Schedule subsidises breast reduction surgery undertaken in private hospitals,4 thereby recognising it as a functional procedure that warrants public subsidy. Access to breast reduction surgery in public hospitals, however, is restricted by state‐specific policies. In Victoria, it is deemed an aesthetic procedure available in public hospitals only for women with a body mass index less than 30 kg/m2 and significant clinical symptoms;5 in New South Wales, breast reduction surgery is classed as a cosmetic surgical procedure to be performed in public hospitals only in cases of severe disability caused by breast size.6 Breast reduction is an excluded procedure (with few exceptions) in Western Australia7 and the Australian Capital Territory;8 in South Australia it is a restricted procedure.9 These differences in access are not compatible with the national right of access to surgical procedures for all Australians “based on their needs, not ability to pay, regardless of where they live in the country.”10

While the clinical effectiveness of breast reduction surgery is documented, high quality evaluations of its cost‐effectiveness have not been published. Cost–utility analysis compares the incremental costs and incremental health outcomes (measured as quality‐adjusted life‐years [QALYs] or disability‐adjusted life‐years [DALYs]) of an intervention with usual practice or a control group. As this analysis provides a consistent unit of outcome measurement (cost per QALY gained), the cost‐effectiveness of different health care interventions can be compared. For this reason, cost–utility analysis is recommended by the Medical Services Advisory Committee (MSAC).11 The primary objective of our study was to determine whether breast reduction surgery in Australian public hospitals is cost‐effective.

Methods

We analysed data collected for a prospective cohort study that included adult women with symptomatic breast hypertrophy (aged 18 years or older) assessed for bilateral breast reduction at the Flinders Medical Centre, Adelaide, during 1 April 2007 – 28 February 2018.2 Participating women who underwent surgery completed assessments before surgery and three, six and twelve months after surgery. A control group of women with breast hypertrophy, who had sought but not yet undergone breast reduction surgery, completed study questionnaires at baseline and twelve months after enrolment.

Health care costs

Direct hospital costs for the surgical intervention were determined from the perspective of the South Australian public health system. Costs data for individual women were obtained from hospital finance departments, based on surgical procedure codes for the surgical admission and all related hospital costs within twelve months of surgery for outpatient clinical care, return‐to‐theatre admissions, and revision procedures. Costs were adjusted for inflation to 2021 Australian dollars.

Health‐related quality of life

Health‐related quality of life was quantified as individual Short Form six dimensions (SF‐6D) utility scores derived from responses to the SF‐36 (version 2).12,13 The SF‐6D defines utility values for 18 000 possible health states of the SF‐36 on the QALY scale (1 = full health; 0 = death).

Cost–utility analysis

The health quality of life‐related effectiveness of breast reduction surgery was measured as QALY gain over twelve months, calculated at the patient level using SF‐6D utility values and the area‐under‐the‐curve method.14 We estimated unadjusted and regression‐adjusted QALYs (for differences in SF‐6D utility scores at baseline).12 For the base case analysis, baseline and 12‐month SF‐6D data were used to estimate QALYs. As we assumed that health‐related quality of life gains would be maintained beyond twelve months, 12‐month QALYs were extrapolated to a 10‐year time horizon. As recommended by MSAC guidelines,11 we applied a discount rate of 5% per year to QALY gains beyond one year. We assumed that the direct costs of surgery were confined to the 12‐month study period, and they were not discounted.

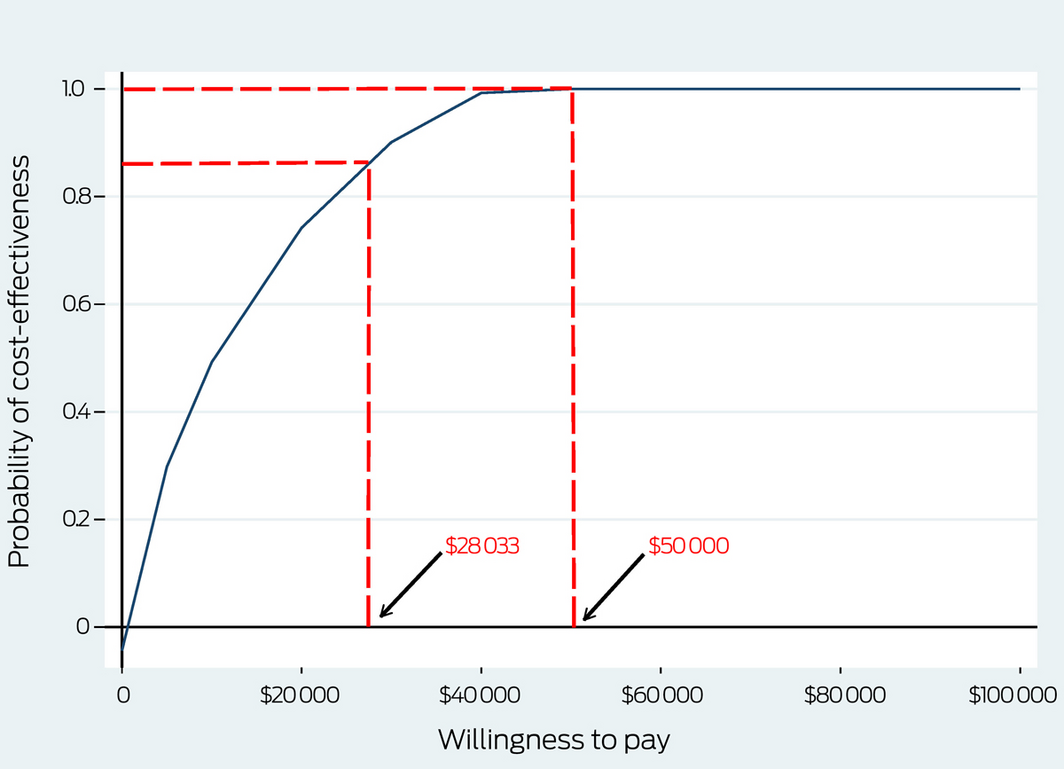

Secondary outcomes of the cost–utility analysis were the incremental costs per QALY gained (the incremental cost‐effectiveness ratio, ICER), defined as the differences in costs between the intervention and control groups divided by the difference in QALY gain. We used published willingness‐to‐pay thresholds of $28 03315 and $50 000 per QALY gained12 for cost‐effectiveness decision‐making. We employed bootstrapping to account for uncertainty related to sampling variation in the ICER; 5000 paired estimates of mean differences in costs and outcomes were derived, and the bootstrapped pairs plotted in a cost‐effectiveness plane. The probability of the intervention being cost‐effective at different willingness‐to‐pay thresholds is presented in a cost‐effectiveness acceptability curve.

Multiple imputation was used to account for any missing cost or outcome values. Imputed values were generated using predictive mean matching.16 A total of 50 multiple imputed complete datasets were generated, and are presented as the base case analysis.

Sensitivity analyses

We tested the robustness of our base case estimates in a series of sensitivity analyses. In the first, we restricted the economic evaluation to complete cases (women for whom complete outcomes information at baseline and 12 months was available). In the second sensitivity analysis, QALY estimates for the intervention group were derived from data for all four time point assessments. In the third sensitivity analysis, we extrapolated 12‐month QALYs to a 40‐year horizon, assuming that the health‐related quality of life gain would be maintained until the end of life (life expectancy for women in Australia: 84.6 years).17 The fourth sensitivity analysis conservatively assumed that baseline control group SF‐6D utility scores were maintained at twelve months.

Statistical analysis

Statistical analyses were performed in SPSS for Windows 25.0 (IBM) or Stata 16. Data for continuous variables are summarised as means with standard deviations (SDs), and differences between groups as mean differences with 95% confidence intervals (CIs). The statistical significance of differences for socio‐demographic variable was assessed in independent samples t tests. Data for categorical variables are summarised as frequencies and proportions, and the statistical significance of differences were assessed in χ2 or Fisher exact tests.

Ethics approval

The study was approved by the Southern Adelaide Clinical Human Research Ethics Committee (references 118.056, 73.17).

Results

Two hundred and fifty‐one women who underwent bilateral breast reduction were included in the intervention group, of whom 209 completed the baseline questionnaire and at least one post‐operation assessment (83%): 191 at three months (91%), 183 at six months (88%), and 193 at twelve months (92%). SF‐6D utility scores were generated for 141 of the 159 participants who completed all four assessments (63%) without any missing responses to SF‐36 items.

In the control group, study questionnaires were mailed to 350 women on the breast reduction surgery waiting list; 160 completed the baseline questionnaire (46%), of whom 124 also completed 12‐month assessments; SF‐6D utility scores could be generated for 119 participants. The baseline demographic characteristics of the intervention and control groups were similar (Box 1).

Health‐related quality of life

The mean SF‐6D utility score for the intervention group was higher at three months than at the baseline assessment, and was similar at the 3‐, 6‐ and 12‐month assessments; the mean value for women in the control group was slightly lower at twelve months than at baseline (Box 2; Supporting Information, table 1). A sensitivity analysis restricted to women with complete outcomes data yielded a similar result (Box 2). In the base case analysis, the mean QALY gain over ten years was higher for the intervention than the control group (adjusted difference, 1.519 QALYs; 95% CI, 1.362–1.675 QALYs) (Box 3).

A larger proportion of smokers (24 of 92, 26%) than of non‐smokers (11 of 117, 9%) had post‐surgical complications, and the mean tissue resection weight was greater for women who experienced complications (1506 g; SD, 974 g v 1192 g; SD, 637 g), Other participant characteristics were not associated with statistically significant differences. The mean change in 12‐month SF‐6D scores was similar for women with (0.29 points; SD, 0.27 points) and without complications (0.31 points; SD, 0.29 points) (Supporting Information, table 2).

Cost–utility analysis

In the base case analysis, the mean total hospital cost for women in the intervention group was $11 857 (SD, $4322) per patient (Box 4); the ICER for the intervention was consequently $7808 per QALY gained (95% CI, $7137–$8040/QALY) (Box 3).

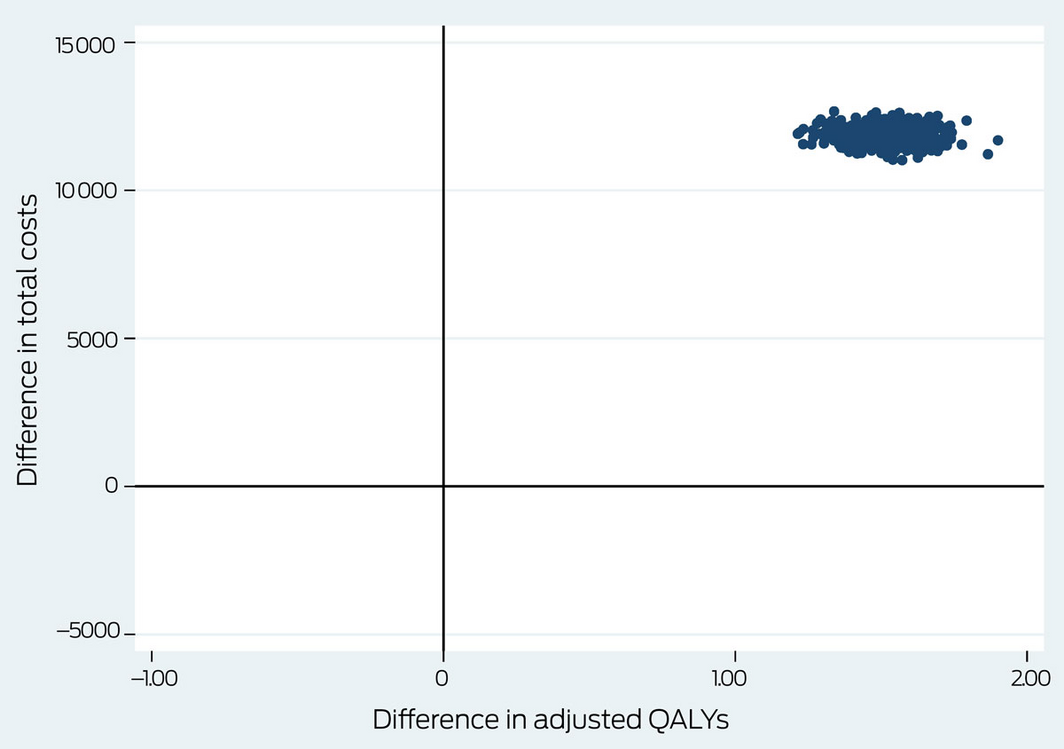

For the base case analysis, all bootstrapped paired estimates of mean differences in costs and outcomes were located in the top right quadrant of the cost‐effectiveness plane, indicating that health outcomes were better for the intervention than the control group, and that costs were higher for the intervention group (Box 5).

The probability of breast reduction being cost‐effective was 88% at the willingness‐to‐pay threshold of $28 033 per QALY, and 100% at $50 000 per QALY (Box 6).

In the base case analysis, multiple imputation was used to estimate missing costs data (13 observations, 6.2%) and SF‐6D utility scores at 12 months (16 observations, 7.7%).

Sensitivity analyses yielded similar results to the main analysis; improvement in outcomes was consistently greater for the intervention than the control group, and the estimated ICERs for the intervention were considerably below the two recommended willingness‐to‐pay thresholds (Box 3).

Discussion

We report one of the most comprehensive economic evaluations undertaken in any country of the cost‐effectiveness of breast reduction surgery for women with symptomatic breast hypertrophy. Few studies have previously assessed its cost‐effectiveness.18,19,20,21,22 Our findings indicate that breast reduction surgery is cost‐effective at implicit willingness‐to‐pay thresholds of $28 033 and $50 000 per QALY gained.

The 10‐year time horizon in our analysis is conservative. In a long term study, we found that the benefits of surgery do not decline over longer follow‐up (up to 12 years),23 suggesting that the cost‐effectiveness of surgery may be even more favourable.

Quantifying the effectiveness of breast reduction as incremental cost per QALY gain facilitates direct comparisons with medical interventions for other chronic health conditions. Assessment of the cost‐effectiveness of orthopaedic arthroplasty procedures in Australia found that both total hip and total knee replacement were cost‐effective, with respective estimated costs of $7500 and $10 000 per QALY.24 Bariatric surgery for the treatment of obesity was found to be less cost‐effective in Australia, but its cost was still below willingness‐to‐pay thresholds.12,15,25 Cost–utility analysis indicated that cochlear implantation was cost‐effective for Australian adults with hearing loss compared with bilateral hearing aids, with an ICER of $11 160 per QALY.26 Laser‐assisted cataract surgery is not cost‐effective compared with alternative medical interventions, including conventional cataract surgery, because of the higher costs of the newer technology.27 In summary, the cost per QALY for breast reduction surgery compares favourably with those for other medical interventions widely accepted in Australian public health care.

Strengths and limitations

A major strength of our study was the use of prospectively collected health‐related quality of life data, and our QALY estimates were based on information supplied by the women affected, not clinician opinion or literature review. In addition, our study assessed costs at the patient level, and took into account factors that influence total costs, including hospital length of stay, in‐hospital complications, and return‐to‐theatre re‐admissions. Further, hospital costs data included expenses incurred after the initial hospital admission, including all hospital outpatient clinic appointments and any revision procedures during the subsequent 12 months. The participation rate in our study was relatively high, and a sensitivity analysis restricted to complete cases yielded similar results, suggesting that multiple imputation did not bias our estimates.

We included all direct hospital costs, but not indirect costs to the participants and their families (such as loss of income because of time off work), primary and specialist care, physiotherapy, or other expenses outside the hospital, nor did it include costs for other relevant hospitalisations. However, indirect costs at baseline would probably have been similar in both study groups and would not have markedly influenced our analysis. In addition, we did not evaluate a randomised clinical trial, and the generalisability of the results of our single‐institution study is unclear. As the women in our study were not blinded to treatment, reporting bias was possible. Estimated differences between the intervention and control groups were based on prospective assessment of health‐related quality of life in both groups at baseline and 12 months. However, including all four assessment time points for the intervention group to estimate QALYs yielded conclusions similar to those of the main analysis; the ICER was indeed more favourable in this analysis, as the marked improvement in intervention group utility scores between baseline and three months increased the area under the curve for QALY calculations.

Conclusion

In our cost–utility analysis, we found that breast reduction surgery for women with symptomatic breast hypertrophy is cost‐effective in Australian public health care; the incremental cost per QALY gained is considerably lower than the implicit cost‐effectiveness threshold. This finding is strengthened by the fact that the probability of the intervention being cost‐effective was high across a range of feasible willingness‐to‐pay values. Our study provides evidence that healthcare systems in all Australian states should support access to breast reduction surgery for both private and public patients.

Box 1 – Baseline characteristics of the intervention and control groups*

|

Characteristic |

Intervention group |

Control group |

|||||||||||||

|

|

|||||||||||||||

|

Number of women |

209 |

124 |

|||||||||||||

|

Age (years), mean (SD) |

42.6 (13.4) |

45.3 (13.1) |

|||||||||||||

|

Body mass index (kg/m2), mean (SD) |

32.7 (6.0) |

32.1 (6.0) |

|||||||||||||

|

< 30 kg/m2 |

71 (34%) |

48 (39%) |

|||||||||||||

|

≥ 30 kg/m2 (obese) |

138 (66%) |

74 (61%) |

|||||||||||||

|

Smoking status |

|

|

|||||||||||||

|

Non‐smoker |

108 (52%) |

78 (63%) |

|||||||||||||

|

Current smoker |

35 (17%) |

14 (11%) |

|||||||||||||

|

Ceased in the past 12 months |

15 (7%) |

5 (5%) |

|||||||||||||

|

Ceased at least one year ago |

47 (23%) |

25 (20%) |

|||||||||||||

|

|

|||||||||||||||

|

SD = standard deviation. * Women who had completed the baseline questionnaire and at least one follow‐up assessment. |

|||||||||||||||

Box 2 – Health utility (SF‐6D) scores for the intervention and control groups, 0–12 months

|

Analysis |

Intervention group |

Control group |

Mean difference (bootstrapped) (95% CI) |

||||||||||||

|

|

|||||||||||||||

|

Base case analysis (imputed cases) |

|

|

|

||||||||||||

|

Number of women* |

209 |

124 |

|

||||||||||||

|

SF–6D scores, mean (SD) |

|

|

|

||||||||||||

|

Baseline |

0.313 (0.263) |

0.296 (0.267) |

0.017 (–0.011 to 0.045) |

||||||||||||

|

3 months |

0.575 (0.287) |

— |

— |

||||||||||||

|

6 months |

0.616 (0.294) |

— |

— |

||||||||||||

|

12 months |

0.626 (0.277) |

0.270 (0.257) |

0.356 (0.322 to 0.390) |

||||||||||||

|

Sensitivity analysis (complete cases) |

|

|

|

||||||||||||

|

Number of women† † |

141 |

119 |

|

||||||||||||

|

SF–6D scores, mean (SD) |

|

|

|

||||||||||||

|

Baseline |

0.314 (0.259) |

0.295 (0.262) |

0.017 (–0.011 to 0.045) |

||||||||||||

|

3 months |

0.570 (0.270) |

— |

— |

||||||||||||

|

6 months |

0.612 (0.280) |

— |

— |

||||||||||||

|

12 months |

0.628 (0.265) |

0.270 (0.256) |

0.356 (0.322 to 0.390) |

||||||||||||

|

|

|||||||||||||||

|

CI = confidence interval; SD = standard deviation. * Completed at least one post‐operation assessment. † Completed four (intervention group) or two (control group) assessments. |

|||||||||||||||

Box 3 – Health economic outcomes (quality‐adjusted life‐years and incremental cost‐effectiveness ratios [ICERs]) over ten years for the intervention and control groups

|

|

Quality‐adjusted life‐years, mean (SD) |

Difference (bootstrapped) (95% CI) |

|

||||||||||||

|

|

Intervention group |

Control group |

Unadjusted |

Adjusted* |

ICER (95% CI) |

||||||||||

|

|

|||||||||||||||

|

Base case analysis (imputed cases) |

4.094 |

2.467 |

1.627 |

1.519 |

$7808/QALY |

||||||||||

|

Sensitivity analyses |

|

|

|

|

|

||||||||||

|

Complete cases only |

4.152 |

2.447 |

1.705 |

1.491 |

$7883/QALY |

||||||||||

|

Four assessment time points |

4.973 |

2.467 |

2.505 |

2.419 |

$4901/QALY |

||||||||||

|

Extrapolation to end of projected lifetime |

8.523 |

5.137 |

3.387 |

3.162 |

$3750/QALY |

||||||||||

|

Control baseline utility score maintained at 12 months |

4.094 |

2.579 |

1.515 |

1.396 |

$8493/QALY |

||||||||||

|

|

|||||||||||||||

|

SD = standard deviation. * Adjusted for SF‐6D utility score at baseline. |

|||||||||||||||

Box 4 – Health care costs per participant over 12 months for the intervention and control groups

|

|

Costs: mean (SD) |

|

|||||||||||||

|

Analysis |

Intervention group |

Control group |

|

||||||||||||

|

|

|||||||||||||||

|

Base case analysis (imputed) |

|

|

|

||||||||||||

|

Number of women |

209 |

124 |

|

||||||||||||

|

Direct cost: hospital stay |

$10 998 ($4208) |

— |

$10 998 ($10 742‒$11 254) |

||||||||||||

|

Outpatient clinic consultation |

$291 ($122) |

— |

$291 ($272‒$309) |

||||||||||||

|

Plastic surgery outpatient treatment |

$569 ($372) |

— |

$569 ($532‒$607) |

||||||||||||

|

Total costs |

$11 857 ($4322) |

0 |

$11 857 ($11 598‒$12 117) |

||||||||||||

|

Sensitivity analysis (complete cases) |

|

|

|

||||||||||||

|

Number of women |

196 |

124 |

|

||||||||||||

|

Direct cost: hospital stay |

$10 888 ($4211) |

— |

$10 888 ($10 295‒$11 481) |

||||||||||||

|

Outpatient clinic consultation |

$291 ($119) |

— |

$291 ($274‒$308) |

||||||||||||

|

Plastic surgery outpatient treatment |

$572 ($361) |

— |

$572 ($521‒$623) |

||||||||||||

|

Total costs |

$11 751 ($4332) |

0 |

$11 751 ($11 461‒$12 039) |

||||||||||||

|

|

|||||||||||||||

|

CI = confidence interval; SD = standard deviation. |

|||||||||||||||

Received 7 April 2021, accepted 12 August 2021

- Tamara A Crittenden1,2

- Julie Ratcliffe3

- David I Watson2

- Christine Mpundu‐Kaambwa3

- Nicola R Dean1,2

- 1 Flinders Medical Centre, Adelaide, SA

- 2 Flinders University, Adelaide, SA

- 3 Caring Futures Institute, Flinders University, Adelaide, SA

We thank the participants for their involvement in the study. Tamara Crittenden holds an Australian Government Research Training Programme PhD Scholarship.

No relevant disclosures.

- 1. Thoma A, Sprague S, Veltri K, et al. A prospective study of patients undergoing breast reduction surgery: health‐related quality of life and clinical outcomes. Plast Reconstr Surg 2007; 120: 13–26.

- 2. Crittenden T, Watson DI, Ratcliffe J, et al; AFESA Research Group. Does breast reduction surgery improve health‐related quality of life? A prospective cohort study in Australian women. BMJ Open 2020; 10: e031804.

- 3. Collins ED, Kerrigan CL, Kim M, et al. The effectiveness of surgical and nonsurgical interventions in relieving the symptoms of macromastia. Plast Reconstr Surg 2002; 109: 1556–1566.

- 4. Australian Department of Health. Medicare Benefits Schedule: item 45523. MBS Online. http://www9.health.gov.au/mbs/fullDisplay.cfm?type=item&q=45523&qt=ItemID (viewed Oct 2021).

- 5. Victorian Department of Human Services. Elective surgery access policy. July 2015. https://www2.health.vic.gov.au/about/publications/policiesandguidelines/elective‐surgery‐access‐policy‐2015 (viewed Jan 2021).

- 6. New South Wales Department of Health. Waiting time and elective surgery policy. Feb 2012. http://www1.health.nsw.gov.au/pds/ActivePDSDocuments/PD2012_011.pdf (viewed Jan 2021).

- 7. Western Australian Department of Health. Elective surgery access and waiting list management policy. Apr 2017. https://ww2.health.wa.gov.au/About‐us/Policy‐frameworks/Clinical‐Services‐Planning‐and‐Programs/Mandatory‐requirements/Elective‐Services/Elective‐Surgery‐Access‐and‐Waiting‐List‐Management‐Policy (viewed Jan 2021).

- 8. Australian Capital Territory Health. Waiting time and elective surgery access policy. July 2016. http://health.act.gov.au/sites/default/files/2019‐02/Waiting%20Time%20and%20Elective%20Surgery%20Access%20Policy.docx (viewed Jan 2021).

- 9. SA Health. Restricted elective surgery policy directive. May 2018. https://www.sahealth.sa.gov.au/wps/wcm/connect/3d568a77‐a030‐437a‐957e‐9b60bb143341/Directive_Restricted+Elective+Surgery_03072018.pdf?MOD=AJPERES&CACHEID=ROOTWORKSPACE‐3d568a77‐a030‐437a‐957e‐9b60bb143341‐mhygh9U (viewed Jan 2021).

- 10. Council of Australian Governments. National healthcare agreement (2022). Sept 2021. https://meteor.aihw.gov.au/content/index.phtml/itemId/740910 (viewed Oct 2021).

- 11. Medical Services Advisory Committee. Technical guidelines for preparing assessment reports for the Medical Services Advisory Committee. Medical service type: therapeutic; version 2.0. Mar 2016. http://www.msac.gov.au/internet/msac/publishing.nsf/Content/0BD63667C984FEEACA25801000123AD8/$File/TherapeuticTechnicalGuidelines‐Final‐March2016‐Version2.0‐accessible.pdf (viewed Jan 2021).

- 12. Brazier J, Ratcliffe J, Saloman J, Tsuchiya A. Measuring and valuing health benefits for economic evaluation. 2nd ed. Oxford: Oxford University Press, 2017.

- 13. Norman R, Viney R, Brazier J, et al. Valuing SF‐6D health states using a discrete choice experiment. Med Decis Making 2014; 34: 773–786.

- 14. Drummond MF. Methods for the economic evaluation of health care programmes. 3rd ed. Oxford: Oxford University Press, 2005.

- 15. Edney LC, Haji Ali Afzali H, et al. Estimating the reference incremental cost‐effectiveness ratio for the Australian health system. Pharmacoeconomics 2018; 36: 239–252.

- 16. Little RJA. Missing‐data adjustments in large surveys. J Bus Econ Stat 1988; 6: 287–296.

- 17. Australian Institute of Health and Welfare. Life expectancy and potentially avoidable deaths in 2015–2017. Updated 2 Aug 2019. https://www.aihw.gov.au/reports/life‐expectancy‐deaths/life‐expectancy‐avoidable‐deaths‐2015‐2017/contents/summary (viewed Oct 2021).

- 18. Araújo CD, Veiga DF, Hochman BS, et al. Cost‐utility of reduction mammaplasty assessed for the Brazilian public health system. Aesthet Surg J 2014; 34: 1198–1204.

- 19. Saariniemi KM, Kuokkanen HO, Räsänen P, et al. The cost utility of reduction mammaplasty at medium‐term follow‐up: a prospective study. J Plast Reconstr Aesthet Surg 2012; 65: 17–21.

- 20. Taylor AJ, Tate D, Brandberg Y, Blomqvist L. Cost‐effectiveness of reduction mammaplasty. Int J Technol Assess Health Care 2004; 20: 269–273.

- 21. Thoma A, Kaur MN, Tsoi B, et al. Cost‐effectiveness analysis parallel to a randomized controlled trial comparing vertical scar reduction and inverted T‐shaped reduction mammaplasty. Plast Reconstr Surg 2014; 134: 1093–1107.

- 22. Tykkä E, Räsänen P, Tukiainen E, et al. Cost‐utility of breast reduction surgery: a prospective study. J Plast Reconstr Aesthet Surg 2010; 63: 87–92.

- 23. Crittenden TA. Quality of life and other outcomes of breast reduction surgery [thesis]. Flinders University, Adelaide; Nov 2020. https://theses.flinders.edu.au/view/5f596e3a‐e41f‐4ca8‐bae8‐6f42d9b936f1/1 (viewed Jan 2021).

- 24. Segal L, Day SE, Chapman AB, Osborne RH. Can we reduce disease burden from osteoarthritis? Med J Aust 2004; 180: S11–S17. https://www.mja.com.au/journal/2004/180/5/can‐we‐reduce‐disease‐burden‐osteoarthritis

- 25. James R, Salton RI, Byrnes JM, Scuffham PA. Cost‐utility analysis for bariatric surgery compared with usual care for the treatment of obesity in Australia. Surg Obes Relat Dis 2017; 13: 2012–2020.

- 26. Foteff C, Kennedy S, Milton AH, et al. Cost–utility analysis of cochlear implantation in Australian adults. Otol Neurotol 2016; 37: 454–461.

- 27. Abell RG, Vote BJ. Cost‐effectiveness of femtosecond laser‐assisted cataract surgery versus phacoemulsification cataract surgery. Ophthalmology 2014; 121: 10–16.

Abstract

Objective: To assess the cost‐effectiveness of breast reduction surgery for women with symptomatic breast hypertrophy in Australia.

Design: Cost‒utility analysis of data from a prospective cohort study.

Setting, participants: Adult women with symptomatic breast hypertrophy assessed for bilateral breast reduction at the Flinders Medical Centre, a public tertiary hospital in Adelaide, April 2007 – February 2018. The control group included women with breast hypertrophy who had not undergone surgery.

Main outcome measures: Health care costs (for the surgical admission and other related hospital costs within 12 months of surgery) and SF‐6D utility scores (measure of health‐related quality of life) were used to calculate incremental costs per quality‐adjusted life‐year (QALY) gained over 12 months, extrapolated to a 10‐year time horizon.

Results: Of 251 women who underwent breast reduction, 209 completed the baseline and at least one post‐operation assessment (83%; intervention group); 124 of 350 invited women waiting for breast reduction surgery completed the baseline and 12‐month assessments (35%; control group). In the intervention group, the mean SF‐6D utility score increased from 0.313 (SD, 0.263) at baseline to 0.626 (SD, 0.277) at 12 months; in the control group, it declined from 0.296 (SD, 0.267) to 0.270 (SD, 0.257). The mean QALY gain was consequently greater for the intervention group (adjusted difference, 1.519; 95% CI, 1.362–1.675). The mean hospital cost per patient was $11 857 (SD, $4322), and the incremental cost‐effectiveness ratio (ICER) for the intervention was $7808 per QALY gained. The probability of breast reduction surgery being cost‐effective was 100% at a willingness‐to‐pay threshold of $50 000 per QALY and 88% at $28 033 per QALY.

Conclusions: Breast reduction surgery for women with symptomatic breast hypertrophy is cost‐effective and should be available to women through the Australian public healthcare system.